Is Buying a Home Still a Good Investment in 2026?

Real estate has a continuous history of being regarded as the best investment for your future and family. However, this view is being challenged globally by several factors that make a home a questionable investment decision. Many are even being forced to question a home as a residence, not an investment.

According to IPX1031, 62% of Americans say buying a home in 2026 feels unrealistic. So, in this article, we look at the honest state of homeownership in the U.S. Then, we delve into the numbers and some approaches that may make homeownership more approachable.

The Honest State of Homeownership Right Now

In the U.S., homeownership is still a goal for the majority of people who do not yet have a home. According to LendingTree, 84% of young non-homeowners want one. The same survey points out that about a quarter have not bought due to low income, and another quarter cite high home prices.

Why Homeownership Feels Unrealistic for Young Americans

Simply put, economic conditions stop half of young Americans of homebuying age from making a purchase. Additionally, more than two-thirds of the cohort that reports being unable to buy for economic reasons also cites high mortgage interest rates.

At the same time, the same Lending Tree survey revealed that more than half of young Americans do not have even a general idea of their budget for buying a home.

First-Time Buyers Are Entering Later

This lines up with NAR data that reveals that the share of first-time homebuyers is at a historic low. The median age for first-time homebuyers is also at an all-time high of 40. That is up from 33 in 2021, demonstrating a worryingly fast shift in accessibility to homeownership.

Essentially, the “normal” age to buy a home has shifted. Young adults want their own homes, but by and large report holding off while they wait for a better personal financial situation and a more homebuyer-friendly economy.

Renters Are Struggling to Save

According to Harvard’s Joint Center for Housing Studies, home prices and elevated interest rates are creating an “affordability crisis.”

It’s not just the young who are affected. U.S. home sales are at their lowest level in 30 years. Many homeowners are highly reluctant to sell their properties, while the financial barriers to buying a new home, whether it’s your first or third, are much higher.

There are a few cohorts dealing with specific barriers to first-time or later homeownership. For many of those who have never owned a home, rent cost burdens are another factor at an all-time high, with half of renters spending more than 30% of their incomes on rent and utilities.

While starter-home initiatives have started producing more low-cost homes, the rewards have only just started to materialize. New home sales have increased only slightly during the last year. However, it’s possible that this trend will slowly change as more starter homes enter the market.

What Has Changed Since 2020

Since 2020, three things have been going on at once:

- Prices have been rising fast

- Mortgage rates have shot up

- Mobility has been reduced as more people stay put and keep their homes off the market

The S&P Cotality Case-Shiller U.S. National Home Price Index went from 212.360 in January 2020 to 332.678 in April 2026.

This appreciation of approximately 57% came as the 30-year fixed mortgage rate moved from a record-low 2.65% in January 2021 to a relatively high 6.43% on July 2, 2026.

For people considering buying a home, low rates were offsetting fast-rising prices for a time. By early 2026, prices and borrowing costs had both risen substantially.

Harvard’s Joint Center for Housing Studies notes that existing-home sales are sitting at three-decade lows while inventories are rising and cost burdens for both renters and owners are continuing to climb. Overall, the market is not frozen, but it is harder to navigate.

The Case for Buying a Home as an Investment

Despite recent financial barriers to buying a home, there are strong reasons to enter the real estate market. High costs are a barrier but are also the result of the long-term value that a home represents as an investment.

Most people understand that homes can build wealth over time. But it’s worth looking into whether the returns are strong, in light of the high costs.

Long-Term Appreciation: What Historical Returns Actually Show

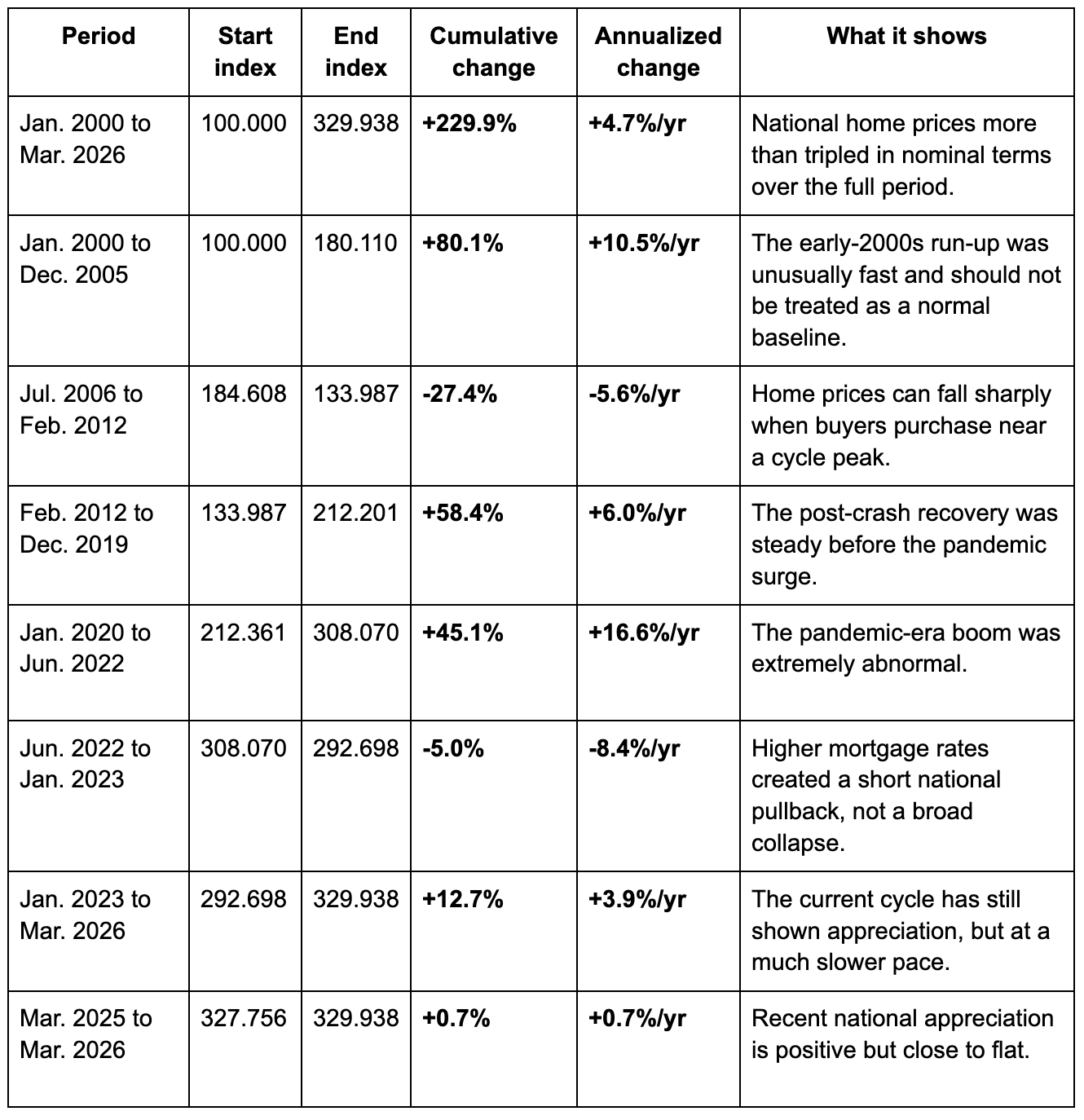

The strongest source for long-term appreciation data for homes is the S&P Cotality Case-Shiller U.S. National Home Price Index, which started in 2000.

To make sense of the data, we’ve broken it down into a few key time periods, starting with the last quarter-century.

Recent national appreciation is positive but close to flat.

For buyers in 2026 onward, there are a few broad lessons in the data.

First, the data does not suggest that every home bought at any time was automatically a great investment. Prices have fallen and recovered in cycles over time, with a consistent growth trajectory. However, that growth was never experienced in a straight line. Instead of focusing on the best specific times to buy and sell, what we can see is that the time horizon matters. Owning a home for decades has consistently been far more beneficial than any short-term strategy.

Second, we can see why the current market feels uniquely difficult. The current high prices reflect years of appreciation due to:

- Limited supply in general

- Strong demand in specific markets

- The fact that housing is both a basic necessity and an investment asset

Equity Building vs. Renting: The Forced Savings Argument

When you buy a home, your mortgage represents both your basic housing costs and a source of long-term savings. Rental payments are for shelter only. So, in this way even if a house is not as comfortably affordable as you’d like, it’s at least forcing you into investing in a form of long-term savings.

Despite the difficulties we’ve discussed above, if you’re thinking about long-term value, there is no comparison between renting and paying down a mortgage. According to the Federal Reserve’s 2022 Survey of Consumer Finances, the median net worth for homeowners was $396,200 that year. By contrast, the median net worth for renters was $10,400.

Of course, there are many ways to contribute to your long-term wealth. But the data points to homeownership being a key component for the vast majority of Americans. Whatever confounding variables contribute to such a disparity in net worth between renters and homeowners, there are some key factors that make homeownership crucial:

- Even if you are not deliberately investing at all, homeownership is the standard passive and natural long-term investment

- Access to equity can give you financial leverage you may not otherwise have

- Historically, owning a home for three decades has outperformed some other common investments

On that last point, consider that long-term homeownership is one of the strongest wealth-building paths for most people. It beats common tools like cash, treasury bonds, and some bond-like alternatives. While homeownership doesn’t beat broad stock-based returns over 30-year periods, or many other investments, consider the fact that it does pay for your shelter and other crucial needs during that time.

Perhaps it doesn’t make sense to compare housing costs like mortgage payments to long-term investment decisions. But that is also why homeownership is such a strong choice: you are investing into a historically reliable asset without having to think hard about investment as a concept.

Homeownership can turn a necessary payment into a wealth-building asset. Value appreciation gets a lot of the attention, but equity is the quieter wealth-producing machine for homeowners.

Inflation Hedge: Why Real Assets Tend to Hold Value

Cash often loses to other investments due to inflation. There are many things that Americans do to hedge against inflation. However, once again, a home is one of the better hedges against inflation, and here’s why.

Real estate is a physical asset with a value tied to:

- Ownership of land

- Construction costs

- Replacement and maintenance costs

- Local housing demand

All of the above factors tend to rise over long periods, with goods, labor, and shelter costs rising, steadily or unsteadily.

Recall that since January 2000, the S&P Cotality Case-Shiller U.S. National Home Price Index rose from 100.000 to 329.938 by March 2026, a roughly 230% nominal increase. During this same period, the Consumer Price Index (CPI) rose by 95.1%.

Then, adjusting for inflation, home prices still rose by about 69% from January 2000 to March 2026. Simply put, housing has a steady history of doing more than keeping up with inflation. There is one caveat: for housing to be a reliable inflation hedge, it’s safer to get a fixed-rate mortgage where your principal and interest stay stable while wages, rents, and prices rise over time.

So, neither Revive nor anyone else is claiming that housing is inflation-proof as an investment. Property taxes, insurance, utilities, maintenance labor, and renovation costs all tend to rise over time. However, inflation can make the original loan balance feel smaller in real terms over a long holding period. This effect can be especially meaningful in high-cost markets like Orange County and California’s major cities.

In summary, if you are able to hold the home long enough for inflation and appreciation to work in your favor, homeownership is normally a good hedge against inflation. It’s also the only inflation hedge that also serves your basic, day-to-day needs in life.

Tax Benefits That Still Apply to Homeowners

Homeowners continue to benefit from several tax advantages. While tax benefits should be near the bottom of the list of reasons to buy a home, they still meaningfully support the decision to buy one.

The various tax benefits you get as a homeowner are attached to:

- Your income

- The size of your mortgage

- Property taxes

- Your tax filing status

- Whether or not you itemize deductions

According to the IRS, homeowners who choose to itemize can deduct mortgage interest on up to $750,000 of qualifying mortgage debt. Married taxpayers filing separately can deduct interest on up to $375,000.

Homeowners who itemize may also deduct eligible state and local taxes, primarily property taxes. The limitations are based on the current SALT cap, which was increased to $40,000, or $20,000 if married and filing separately, subject to income limitations, for the 2025 tax year.

When selling your primary residence, you may also qualify for a large capital gains exclusion. If you’re an eligible homeowner, you may qualify for an exclusion of up to $250,000 of gain from income or up to $500,000 for married couples filing jointly.

Tax benefits are more valuable when you itemize. Many taxpaying homeowners take the standard deduction, meaning:

- Mortgage interest

- Property tax deductions

However, don’t assume that the full deduction will equal cash savings. The point is that there are simply opportunities for homeowners to save in taxes while building equity that aren’t available to renters. Be sure to consult a qualified tax professional before relying on any deductions.

The Case Against Buying a Home

In this economy, the case against buying a home is stronger than usual. That doesn’t mean that homeownership is a bad goal, just that the economics don’t align as strongly for it as during many other points in the past. This is particularly true if you’re looking at a second home as an investment; many of the benefits we covered above are partially mitigated.

In this section, we look into the negatives associated with buying a home so you can make a more informed decision.

The Real Cost of Homeownership

Down payments and mortgages represent the upfront cost, but there is a wider category of expenses to pay when you buy instead of renting:

- Property taxes

- Homeowners insurance

- Maintenance and repairs

- Utilities

- HOA dues where applicable

- Closing costs and future selling costs

These costs all change your investment math. Homes appreciate over time, but homeownership costs reduce your real return.

If your home doesn’t appreciate enough or you end up selling too soon, the real cost of homeownership starts to cut into your financial upside. Consider these factors when doing the math so you understand the risk.

The question goes beyond “Can I qualify for the mortgage?” and moves on to “Can I comfortably own this home after closing?”

Short-Term Buying in High-Cost Markets Can Destroy Wealth

The upsides of homeownership that we explained above rely on a typical homeowner’s logic. If you buy a home for the security of owning your home while building and maintaining personal wealth, you get the greatest long-term benefits.

However, there are some investment decisions that make far less financial sense. Investment purchases may not always make sense, especially short-term purchasing decisions in high-cost markets. In a real estate market like Orange County’s, the economic logic favors decisions that are centered around long-term value.

Why?

Buying a home is risky if you buy it with the goal of selling it in a few years. Over time, returns are stable. But there are many short-term turnaround cases where, even if you sell at a higher price, the costs add up and your realized profit is negative or barely breaking even.

Closing costs, selling costs, repairs, remodels, and even market fluctuations can add up and work against you. Also, high-cost markets like Orange County make the break-even point longer with higher transaction costs.

For the average homeowner, it’s easier to secure a good investment when you let the market go through complete cycles.

Opportunity Cost: What Else Could That Down Payment Do?

The sunk-cost fallacy is not always totally fallacious. Down payments are substantial, especially in the 2026 housing market. In many cases, that level of investment could be invested for higher returns in:

- Stocks

- Bonds

- Business images

- Retirement accounts

These other options have the capacity to offer higher returns over a decades-long period. Often more importantly, they offer higher liquidity as well.

So, buying a home still makes a lot of sense, especially when you consider how basic daily needs converge with a proven long-term investment. But the real comparison is not between buying a home and doing nothing. The argument is between a long-term investment in a home and long-term investments in potentially more profitable categories.

Market Timing and the Liquidity Problem

Real estate is relatively stable and has demonstrated steady and reliable long-term growth. But from a viewpoint that focuses purely on financial benefits and sets aside lifestyle considerations, the liquidity problem comes into play.

Real estate does not sell quickly, easily, or without additional costs. There is always risk when holding a home. That risk quickly and often brutally comes into play in situations like:

- Major life changes

- Job-forced moves

- Divorce

- Sudden income loss

- New and sudden family needs

What Matters More Than the Market: Your Personal Situation

Looking at the arguments for and against making homeownership a priority, it quickly becomes clear that your personal situation is the most important factor.

Personal circumstances often make homeownership unwise or even unrealistic. Under other personal circumstances, it may be an even more important goal.

In this section, we cover the most decisive factors when considering entering the real estate market.

The "Are You Ready?" Checklist

The first considerations need to surround personal preparedness. Homeownership involves far more personal responsibilities when compared to renting or living in others’ homes. It involves more stress and accountability, so it’s worth considering whether you are ready for the mental and emotional cost first.

Beyond the most personal considerations, homeownership is also a substantial financial decision. The precise cost depends on your credit. Determining whether buying a home is a financially responsible decision requires you to consider:

- Credit

- Savings

- Stability

- Timeline

The goal is not to buy as soon as possible. Instead, it’s easiest to buy when the decision supports your life, your finances, and your long-term wealth-building plan.

How Long You Plan to Stay Is the Most Important Variable

When you consider the data, you once again see how much length of time matters when looking at a home as an investment.

According to the CFPB, closing costs typically add up to 2% to 5% of the home’s purchase price, not including the down payment. That means when you buy the home, you start one step behind as appreciation and equity haven’t built yet.

When it comes time to sell, you normally face:

- Agent costs

- Repairs

- Concessions

- Escrow

- Title

- Transfer tax

- Assorted prep and moving costs

During the first few years, your mortgage repayments mainly go toward interest. Equity builds up slowly, leaving you with less wealth at the start. During that time, a market dip can really hurt. Over time, appreciation and equity combine for better wealth building. Historical data shows that time matters more than timing.

The S&P Cotality Case-Shiller index shows national home prices at 329.938 in March 2026, with the index set to 100 in January 2000. Short-term, consider how long a buyer near the 2006 peak would have had to wait for the national market to recover.

As time has gone on, more homeowners are reacting to these trends. The NAR’s 2025 Profile found that the median expected tenure in a purchased home is now 15 years. The typical seller had owned their home for 11 years, another record at the time. By contrast, from 2000 to 2008, sellers typically stayed only 6 years.

If the resale window is too short, you also sacrifice tax benefits. To qualify for the main home sale exclusion, the IRS generally requires you to own and use the home as your main residence for at least 24 months during the five years before selling.

The Break-Even Timeline in High-Cost Markets Like Orange County

The break-even timeline is usually longer in high-cost markets like Orange County.

In Orange County, the cost to buy and sell is higher. Closing costs often fall near the higher side of the 2% to 5% of purchase price range on their own. Then you need to factor in future selling costs, maintenance, insurance, taxes, and possible HOA dues.

FHFA data for Orange County as a whole is unspecific. However, FHFA data for the Anaheim-Santa Ana-Irvine market shows that home prices rose from 132.94 in Q1 2000 to 568.91 in Q1 2026, a gain of about 328%.

However, appreciation has been comparatively slow recently. Appreciation was 1.4% from Q1 2025 to Q1 2026.

The simple takeaway is that in Orange County, it takes time for the numbers to work in your favor. The longer you can hold on, the better.

Is Now (2026) Actually a Decent Time to Buy?

There are no signs that home prices are going to drop, but interest rates may dip modestly. More importantly, there are some changing market dynamics that may work in your favor if you’re looking to buy.

Buyers May Have More Leverage in 2026

Several real estate market factors have converged to make buying a home more attractive in 2026:

- Higher inventory

- Greater average time on the market

- Ultimately, more negotiating power for homebuyers

During the pandemic, buyers were bogged down by bidding wars and limited options. This has been changing during more recent years. Expanding inventory means less pressure and more options and leverage in your hands.

Also, prices have been stabilizing. While they are still rising and show no signs of going down, the skyrocketing has stopped and shows no signs of returning. 2026 is a good year to follow housing prices and shop around without pressure to buy before dream home options become unaffordable.

Interest rates are still high, but some projections show a possible dip below the 6% mark in 2026. Even small rate changes can make a noticeable difference in your monthly payments.

What Mortgage Rate Forecasts Suggest for Late 2026 and Beyond

Mortgage rates may improve, but it does not currently make sense to plan a house purchase around a major drop. Freddie Mac reported the 30-year fixed-rate mortgage at:

- 6.43% as of July 2, 2026

- Down from 6.49% the week before

- Down from 6.67% one year earlier

Fannie Mae’s June 2026 forecast projects the 30-year fixed mortgage rate at 6.4% for Q3 and Q4 2026, then around 6.3% through most of 2027.

Why Waiting for the “Perfect” Market Usually Backfires

While lower rates can make a home purchase more affordable, forecasts cannot pin down a precise, perfect moment. There is no point waiting for a sweet 4% or 3% mortgage. It’s also probable that your personal circumstances will change over time. The intersection of “perfect” personal finances and a “perfect” market is usually not worth waiting for. You can also add changes to inventory and competition, which are affected by even more factors.

When rates fall, you will be among many others who rush back to the market. In such a case, you may end up with less negotiating power. It’s usually better to wait for something good over something perfect.

Most of the time, the better strategy is to buy when the numbers work for:

- Your life

- Your timeline

- Your long-term plan

Homeownership as Investment vs. Homeownership as Home

Homes are different from stocks or other investments because you live in them. Your returns can’t be calculated by appreciation alone. Homes provide:

- Stability

- Equity

- Predictable housing payments

- Control over where you live and your lifestyle

So, it makes sense to ask bigger-picture questions when considering homeownership. Instead of “will my new home appreciate in value?” you can ask “will my new home support my life and my long-term financial planning?”

The Wealth-Building Reality for Most American Homeowners Over 30 Years

Homeownership increases wealth primarily through:

- Long-term value appreciation

- Mortgage principal paydown

- Inflation progressively reducing the burden of fixed, long-term debts

We also have the figure we mentioned earlier that demonstrates the median homeowner has over 38 times the net worth of a renter or other non-homeowner.

None of this suggests that buying a home on its own is a guaranteed path to creating wealth. However, such a strong relationship between homeownership and household wealth does strongly suggest that:

- Homeownership is a key component of wealth-building for the average American

- Homes are relatively stable investments, particularly for 30-year or longer periods

- Buying a home often kills two birds with one stone by providing housing and a strong long-term investment

Why Where You Buy Matters as Much as When

The “location, location, location” phrase is accurate. Real estate is a local asset, with its value tied closely to the surrounding physical and economic environment. National and local datasets are useful, but important data is often between the lines.

A home’s location affects:

- Appreciation potential

- Resale demand

- School and job access

- Commute patterns

- Insurance and tax costs

- Renovation value

- Future buyer demand

Also remember that while timing the market can be hard, choosing the right location is a great way to hedge your bet in the long term. This is why the “right home” is not always the cheapest, but is normally the one that combines affordability with location, condition, and resale potential.

Orange County Real Estate as a Long-Term Investment: What the Data Says

Overall, Orange County is a more expensive market where long-term appreciation has historically been strong.

The FHFA’s Orange County price index shows that OC home prices rose by 295.98% between 2000 and 2025. In some cities, appreciation has been stronger. A related FHFA quarterly, the Anaheim-Santa Ana-Irvine index, revealed that the series of three cities together experienced 327.9% growth from Q1 2000 to Q1 2026.

This upside contrasts with a reduction in affordability. Data from Census QuickFacts shows Orange County’s median owner-occupied home value was $962,600 for 2020-2024. Median ownership costs, including mortgage payments, were $3,385, while median gross rent was $2,434.

Thinking About Buying or Selling in Orange County?

Buying a home remains a strong long-term investment choice in Orange County and elsewhere. However, your returns are more likely to be favorable when the numbers, timeline, and broader strategy make sense.

How Revive Helps Buyers and Sellers Get More from Their Investment

Revive helps homeowners understand the full value of their properties before they make a big decision.

Whether you’re preparing to sell, evaluating a renovation, or preparing to buy, it’s crucial to understand how homes perform over time. Revive’s team brings data, strategy, and local insight to this process.

Explore Our Resources for OC Homeowners

We offer extensive educational and practical resources for Orange County homeowners. Our publications cover home values, market trends, renovation opportunities, and selling strategies that can help you protect and grow your investment.

Talk to Our Team Before You Make Your Next Move

How much is your home's worth?

Get your personalized estimate today.

I’m a dedicated professional with over 8 years of experience in real estate, helping clients navigate the market with confidence and clarity. I take pride in building strong relationships and guiding people through each step of the process with transparency, responsiveness, and a a client-focused approach. Outside of work, I enjoy spending time with my wife and two kids, staying active, and being outdoors.

Recent articles

Rismedia.com

Inman.com

Housing Wire